BLOG

How Much Is Your Debt Really Costing You?

March 12, 2020

We firmly believe that one of the most important aspects of a person’s life is understanding their personal finances. Specifically, understanding and minimizing their debt. There’s a reason we feel so strongly about this:

Not understanding your debt can set you back thousands of dollars without you even realizing it.

Let’s be honest, people go into debt all the time and for good reason. You want to go to college so you take out student loans to pay for classes. You got married and want to buy a house so you save for a down payment and finance the rest with a home loan. Your car breaks down so you want to buy a new, reliable one. You take out a car loan and buy a newer model that will last for 10-20 years.

As long as you’re responsible and not living wildly outside of your means, these are all legitimate expenses. There is nothing wrong with taking out a loan to pay for things that you can’t pay for in cash. The problem, however, is the anglerfish.

Let’s take a look at how much your debt might really be costing you.

What’s an anglerfish?

An anglerfish is a deepwater fish known for their freaky appearance and (more famously) for luring their prey in with a bulb at the end of their dorsal fin that lights up.

Anglerfish, since they live in the deep ocean where it’s incredibly dark, lure unsuspecting fish in with their bright dorsal fin. Fish swim up curiously and then when they get close enough, they’re gobbled up by the anglerfish. Are those fish dumb for swimming up to the light? Not really! They couldn’t see the anglerfish and were just exploring around. They didn’t know any better and didn’t realize their mistake until it was too late.

So what does this have to do with you, your finances, or your debt?

It’s relevant because, in the world of finance, there are people, and institutions, that act like anglerfish. Some (not all!) people working in the personal world are known for their predatory tactics. They deliberately try and take advantage of trusting people who don’t know any better.

In fact, you might have even heard of them before. These types of people are commonly referred to as loan sharks. However, we prefer the term anglerfish for two reasons:

- Sharks are the biggest, baddest predators in the ocean. Everyone knows what a shark is and know to steer clear when one comes by.

- Anglerfish are sneaky. They lure in prey with something bright and shiny and take advantage of curious fish.

Loan sharks are lenders that lend money at extremely high (sometimes illegal) rates of interest. When someone goes to a loan shark for money, the loan shark happily provides it at an interest rate that is drastically higher than what other lenders charge. That person doesn’t realize that the rate is incredibly high. They just simply don’t know any better and happily sign on the dotted line. The anglerfish has another victim.

Just like our example earlier, are these people dumb for getting taken advantage of? Not really! They’re just exploring around in the dark and don’t know any better. They trust the lender to have their best interests at heart.

When your mechanic tells you you need a new carburetor, you probably listen. When your dentist says you need a crown put in, you listen. Why would you not listen to a financier when they tell you what you need to pay in interest?

So the interest rate on my loan is high, so what?

Paying a high-interest rate is a very big problem. As we mentioned earlier, there are a lot of things that you take out loans for. For each of these loans, you’re paying interest. Some examples of things that you’re probably currently paying interest on are:

- Your mortgage

- Student loans

- A car payment

- A new iPhone

- Credit card payments

If you’re currently paying any of these, you’re paying interest as well. If you’re paying an interest rate that is higher than it should be, that means that the amount of money your paying back is exorbitantly higher than it should be. In the world of finance, decimals and small percentages mean a lot. The difference between 1% and 2% is gigantic. Entire trillion-dollar banking segments are based on collecting 1% here and there. The difference between 2% and 6% is a catastrophe. Consider the following example. You go to buy a house and take out a loan similar to the below.

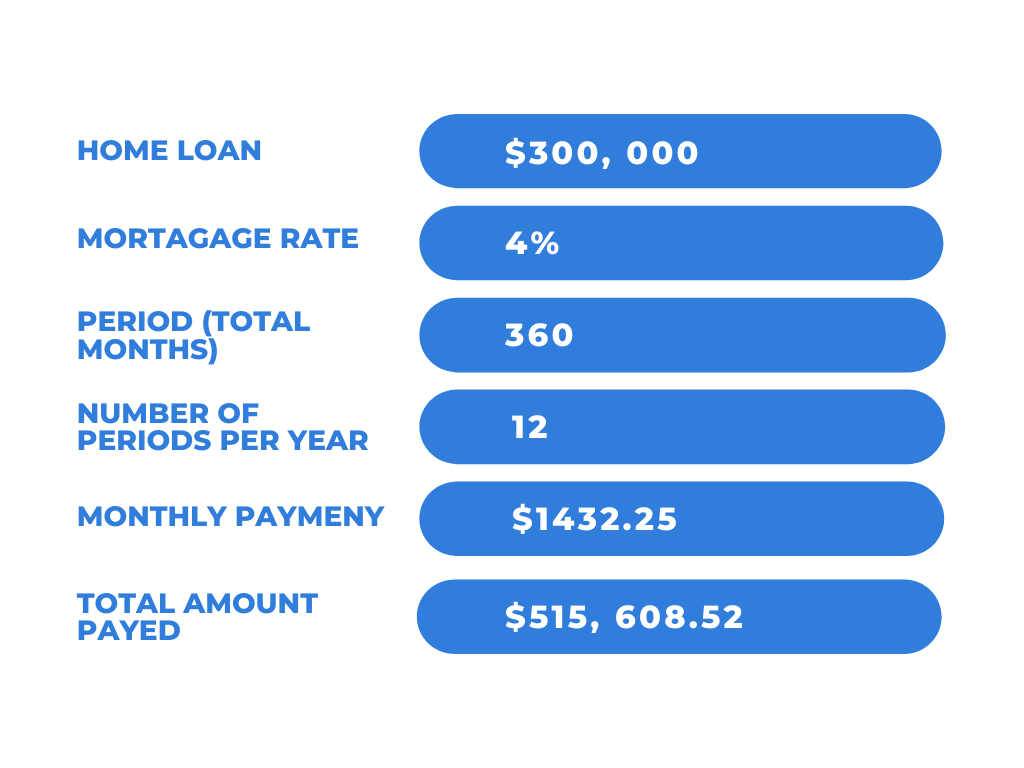

A loan of $300,000 at a rate of 4% over 30 years (360 months). Ultimately you’ll pay $515,608 for the house. That’s $215,608 more than you borrowed. This might seem unfair but unfortunately, that’s the price you pay for borrowing money. Let’s take a look at the same example with a slight tweak.

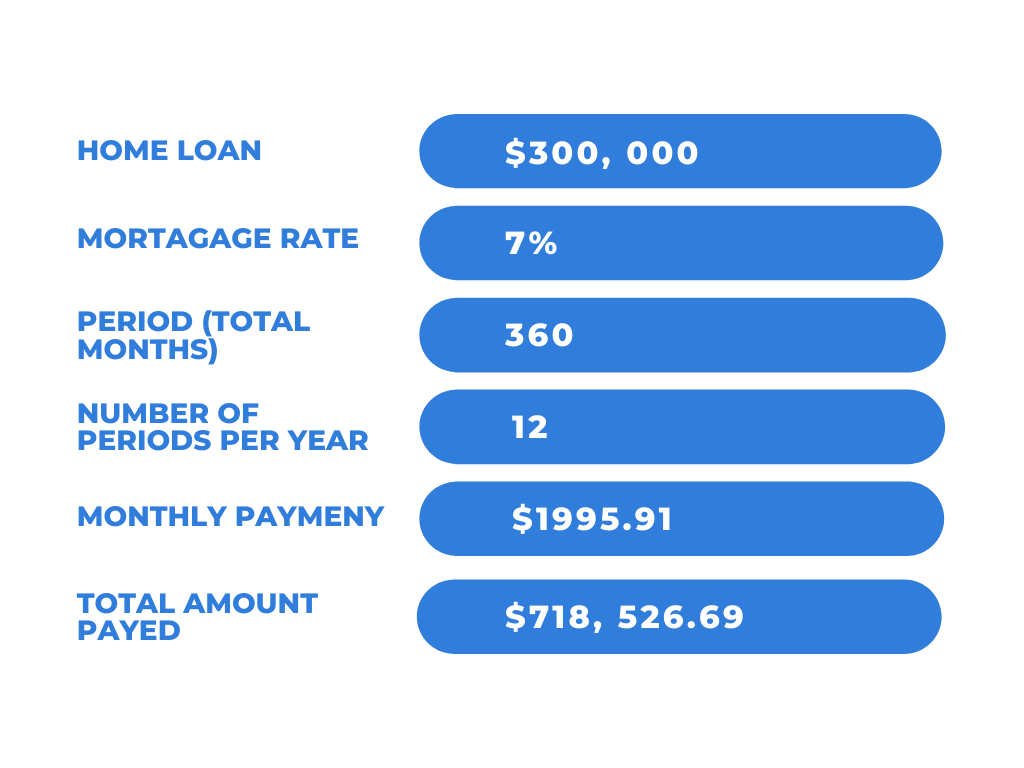

Everything is the same except for one thing: the interest rate. In this example, you paid 7%. By raising the rate just 3% you’re now paying $415,526 in interest!! You need to pay back more than double what you’re borrowing just because of 3%. This is where loan sharks make their money.

As we mentioned, most fish get eaten simply because they don’t know any better. Before we examine solutions you can take to make sure you’re not overpaying, let’s take a look at how loans work. This way the next time you see a shiny light bobbing in the darkness, you’ll know better and quickly swim away.

How loans work in a nutshell

Banks (lenders) make money from loaning money to people who need it. They give you money to buy a house, start a business, buy a car, etc.. In return, you pay them that money back plus extra through what’s called interest.

When you make a payment on a mortgage or similar payment, you’re actually making two payments. You’re paying back the interest as well as paying down a small part of the principal (original amount you borrowed). If you can’t pay the bank back, or default on your loan, the bank is essentially out of luck and loses money.

The bank’s business is in making profitable loans to people they think will be able to pay them back. That’s why they use metrics like credit scores, interview you, and ask for lots of information before approving you for a loan. The bank wants to make sure you will pay them back.

Now that you’ve got a baseline knowledge of how banks make their money, let’s look at what some of your steps as a consumer should.

What should I do?

If you haven’t already, go to the websites of people who have loaned you money.

- Find their website and learn your login information

- Figure out how much you owe

- If you can’t find it on their website, call or email them

- If it’s a bank, go inquire in person

- Learn what interest rate you’re paying and when your loan should be paid off

What you’re doing here is taking control. Taking responsibility for your outstanding debt is the first step. Once you know how much you owe, who you owe it to, and what you’re paying in interest you can take other steps to attack it. This is the most important step because this is where you’ll learn if you’ve been snatched by an anglerfish.

Example:

We had a client who came to us one time just to get an understanding of her financial situation. She didn’t spend a lot of money, made a decent income, and the only debt she had was her outstanding student loans. Not in bad shape! However, we quickly uncovered something that she wasn’t aware of.

When she graduated from college, she was suggested into a repayment plan by her loan provider. The loan provider phrased the plan as one of the most common ways to pay because it had the smallest monthly payment. Since they recommended it, she signed up. “A low monthly payment will help me out and I’m still making progress towards paying it off!” Sound reasoning!

Once she had her automatic deposits set up there was no need to look into it again and a few years passed. She thought she had been making solid progress on repaying the loan but was met with unpleasant news. The repayment plan that she had signed up for turn out to be an interest-only loan repayment plan. So while her monthly payments were low, she had not actually paid off any of her principal and was no closer to paying off her loans than she was when she graduated. Ouch.

This is just one example of how innocent people can be taken advantage of without even realizing it. If she hadn’t come to us (or another advisor) she might have never realized and another 10 years could pass.

Ensure you’re paying market rates

We recommend prying into your outstanding debt to guarantee that you’re paying a normal rate of interest. Remember, you can’t avoid paying interest. It would make no sense for a bank to loan you money without interest. We just want to avoid paying a rate that’s too high.

As a rule of thumb, here are a few average rates of interest:

- The average interest rate for a mortgage: 3.5-4.0%

- The average interest rate for an auto loan: 5.0%

- The average interest rate for a credit card: 20.0%

- The average interest rate for student loans: 5.0-6.0%

These rates are just averages and will be different for everyone. Not everyone gets offered the same interest rates because of things like your credit score, your income, your financial history, your age, etc..

However, if you find out that you’re paying significantly higher than any of these rates, contact us or a financial advisor immediately. Even if you’re midway through repaying the loan, there are usually always opens to refinance and save money. If you remember our mortgage example from earlier, if you’re paying just a few percentage points too high in interest, it could mean thousands of dollars out of your pocket.

We hope that you found this valuable! Even if you’re not overpaying in interest, now you can take this knowledge with you. The next time you apply for a loan, remember to get offers from a few vendors. Multiple offers will reveal what the market (or average) rate that you should be paying. You can also examine different rates online to compare the best ones.

If you enjoyed reading this, please subscribe below to get alerted of new posts that we publish! If you have further questions, please send us an email or explore the rest of our website!